The coffee was lukewarm. The air hummed with the drone of earnest executives discussing… well, the future of software, naturally. But this wasn’t just another tech conference; it was Stripe Sessions, and the buzz wasn’t entirely about generative AI making everything a commodity.

Look, we all know AI is the flavor of the month. Every startup, every legacy player, is slapping an ‘AI-powered’ sticker on their product. The fear, of course, is that AI will commoditize software so thoroughly that features become meaningless. But here’s the dirty little secret the suits at Stripe Sessions were whispering: vertical SaaS platforms have a secret weapon. It’s not more code. It’s deeper integration.

The AI Hedge Fund

Concerns about AI eating software businesses are valid. But vertical SaaS companies aren’t just selling software; they’re selling solutions embedded deep within specific industries. Toast’s Elena Gomez put it plainly: “The companies that win in vertical SaaS are the ones that stay deeply embedded in their customers’ worlds and never stop listening.” Pure AI can’t do that. Not yet, anyway.

And how do you get more embedded? Payments. Obviously. It’s the lifeblood of any business. As AI makes features replicable, payments become the sticky glue holding a platform to its customer’s financial operations. We’re talking transactions, revenue tracking, cash flow management – the stuff that actually matters to a business owner trying to stay afloat.

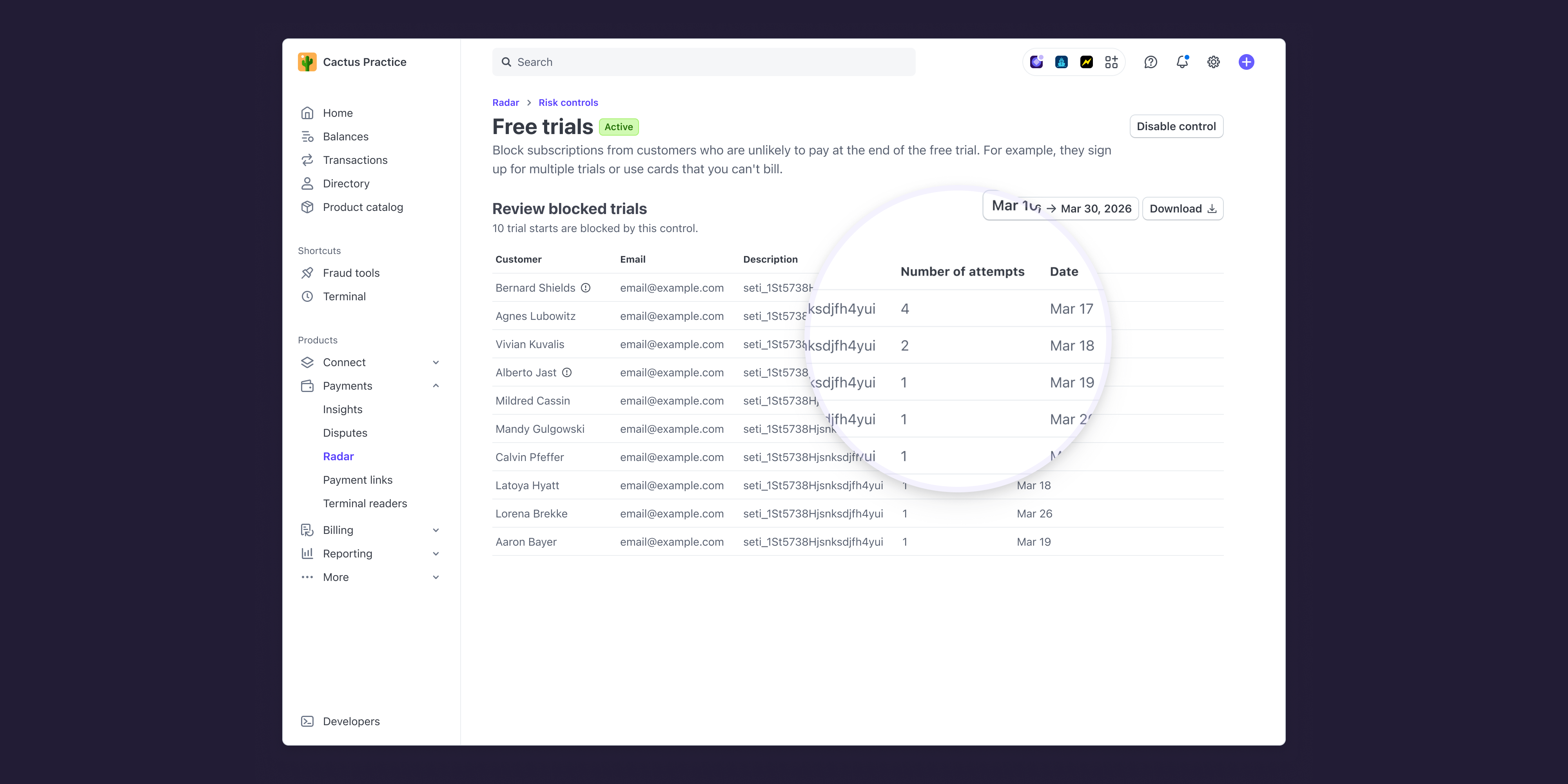

Stripe data shows median payments adoption climbing from 27% in 2024 to 40% in 2025. Not exactly a runaway train, is it? But the top performers? They’re hitting 80%+. How? By making payments a company-wide obsession. “Starting with the ‘why’ is really important,” advises Catherine Beley of GlossGenius. It’s not just about Gross Payment Volume; it’s about growing ARR for the entire company. This isn’t just a product feature; it’s a revenue strategy that permeates sales, onboarding, and customer success.

Fullbay’s Phil Acree even bakes payments into sales compensation. Imagine that: sales reps actually incentivized to talk about payments. Wild.

The payoff is hefty. Tidemark estimates an extra $4,200 in ARR per customer adopting embedded payments. And churn? Platforms with embedded financial products see 11% lower annual churn. Multiproduct strategies? 49% faster revenue growth. Ben Brideaux of Nextech nails it: “A real opportunity for payments leaders is that second-order effect on other revenue within your business. If you can increase retention rate and net dollar retention, you start to see these compounding effects.” It’s about building a sticky ecosystem, not just a feature set.

Building the Moat: Beyond Just Money

Once payments are in the bag, the door swings open to even more offerings. Shopify is the obvious behemoth, offering everything from capital to charge cards. Toast started with POS and now offers payroll, bill pay, and capital. It’s a virtuous cycle of integration.

Obi Omile, CEO of theCut, a barber booking app, saw this firsthand with Stripe Capital. He sent out offers and within 24 hours, 167 barbers had accepted $788,000 in financing. “Barbers were accepting offers within three to four minutes of receiving the email.” The barbers used the capital for new equipment, seasonal lulls, and advertising. The consistent feedback? It helped them grow, build resilience, and expand. This is how you build loyalty.

The moat isn’t solely financial, either. Moxie embeds compliance tools for medspas, ensuring they don’t lose their licenses. Slice negotiates wholesale rates on pizza boxes for restaurants. These are services that AI-native newcomers can’t replicate from day one. They require industry-specific knowledge and established relationships.

The Data Dilemma and AI’s True Role

For all the talk of AI, a significant hurdle remains: data. Most vertical SaaS platforms struggle to access and act upon their own data effectively. While AI can analyze vast datasets, its effectiveness hinges on the quality and accessibility of that data. “Many vertical SaaS providers have customer data locked away in disparate systems, making it impossible for AI to provide meaningful insights,” notes one executive (anonymously, of course).

This is where AI can play a role, but it’s less about creating killer features and more about enhancing the embedded experience. Think AI-driven fraud detection within payment systems, intelligent forecasting for lending decisions, or personalized compliance nudges. It’s about AI augmenting the core value proposition, not replacing it.

The PR Spin vs. The Reality

Stripe’s narrative is compelling: AI is here, embrace it by embedding financial services and deepening operational ties. It’s a smart play for Stripe, naturally. But let’s not confuse this with a universal panacea. For many vertical SaaS companies, the journey to strong embedded finance and operational integration is fraught with technical challenges, regulatory hurdles, and the sheer difficulty of shifting company culture.

The PR spin highlights the successes – the GlossGenius adoption rates, the theCut Capital uptake. The untold story is the painstaking work, the iterative development, and the strategic imperative to move beyond just a feature set. The companies that are truly winning aren’t just riding the AI wave; they’re building deeper, more resilient ships by integrating financial and operational services, making them indispensable. This is the true differentiation in a post-AI world.

Is This Just About Payments?

No, it’s about more than just payments. While embedded payments are a critical first step, they open the door to a suite of financial services and operational tools that create a much stronger competitive moat. The goal is to become an essential part of a customer’s daily operations, making the platform “sticky” and difficult to replace.

How Does AI Fit Into This Strategy?

AI isn’t the primary driver of differentiation for vertical SaaS in this context; instead, it’s an enhancer. AI can improve the embedded experience by providing better data insights for lending, enhancing fraud detection in payments, or offering personalized compliance recommendations. The core strategy remains deep integration, with AI augmenting that value.

What Is Vertical SaaS?

Vertical SaaS refers to software-as-a-service solutions designed for a specific industry or niche, rather than a broad market. Examples include software for restaurants, salons, construction, or automotive repair. These platforms often offer specialized features tailored to the unique needs and workflows of their target industries.

Will This Replace My Job?

For software developers, this trend suggests a shift in focus. The demand will likely grow for developers skilled in building integrated financial products, understanding industry-specific workflows, and potentially applying AI to enhance these embedded services. It’s less about replacing jobs and more about evolving skill sets within the industry.