The faint hum of a server farm, a silent symphony of algorithms processing intent, execution, and credit, is the new sound of commerce.

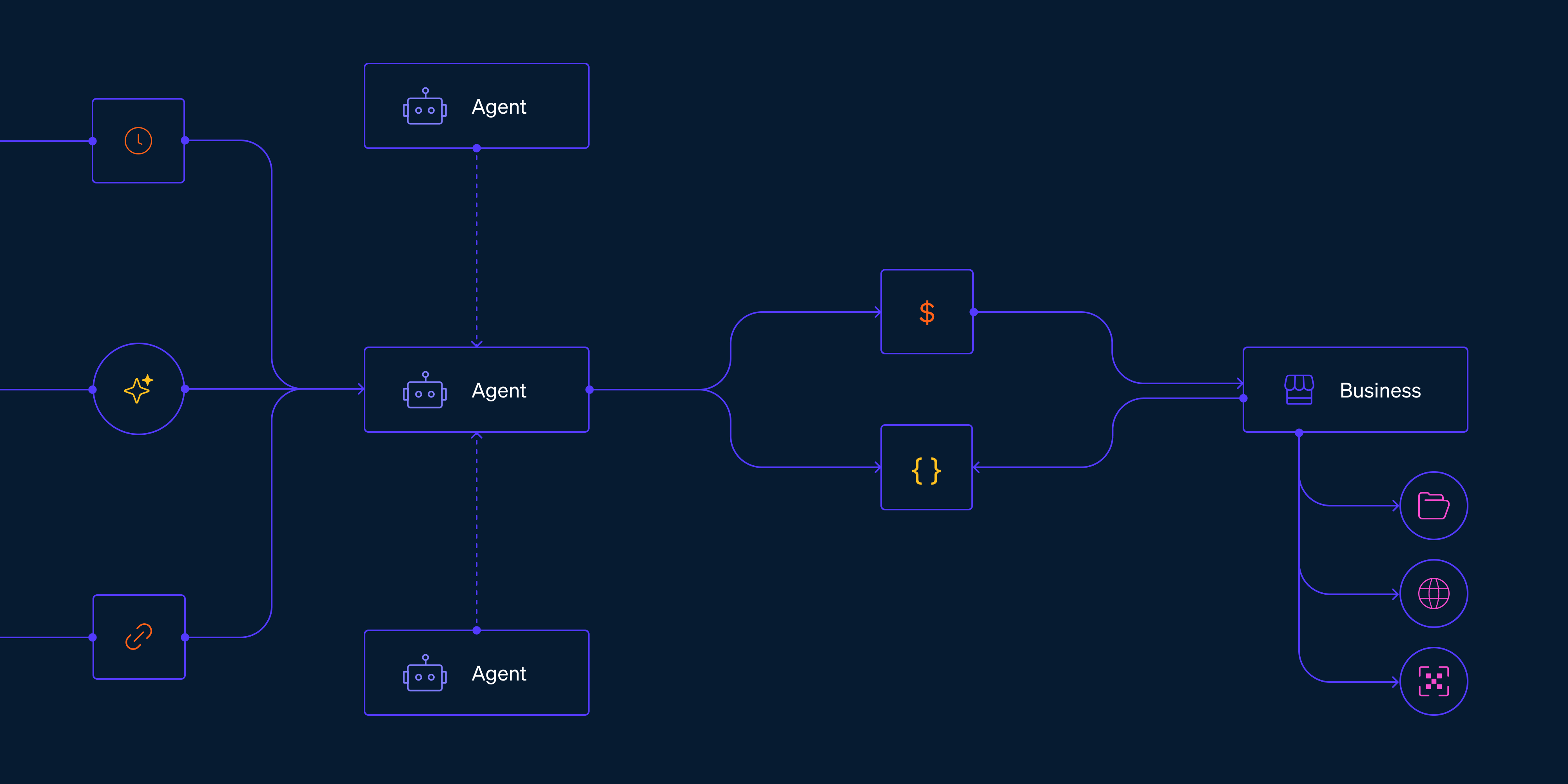

We’re not just talking about faster payments anymore. We’re witnessing a fundamental architectural shift in how transactions are conceived and executed, driven by the rise of what’s being dubbed agentic commerce. It’s the sophisticated integration of artificial intelligence directly into the payment flow, not just as an analytics tool, but as an active participant. Companies like Stripe, American Express, and Affirm are no longer content with simply facilitating transactions; they’re building systems that can understand intent, initiate execution, and dynamically adjust credit, all in near real-time.

Think about it. For decades, the payments stack was a series of largely disconnected layers. You had your intent – the customer deciding to buy something. Then you had execution – the actual movement of money. And somewhere in between, or perhaps as a separate gatekeeper, was credit – the authorization of that purchase. These were distinct processes, often requiring manual intervention or rigid rule sets to bridge the gaps.

Agentic commerce aims to collapse those layers, making the entire process fluid, intelligent, and — crucially — actionable. It’s about creating AI agents that don’t just process data but can reason with it, acting autonomously to achieve a commercial outcome.

Stripe’s Gambit: Making AI a Player, Not Just a Passenger

Stripe, a company that has built its empire on making the developer experience of payments frictionless, is at the forefront of this push. Their work on the Agentic Commerce Protocol (ACP), developed in collaboration with OpenAI, isn’t just about enabling AI systems to make purchases. It’s about establishing a universal language for commerce that AI agents can understand and speak. This means that instead of every merchant needing bespoke integrations for every AI tool their customers might use, there’s a standardized way for agents to interact with the payment infrastructure.

“The firm is trying to normalize the idea that agents will increasingly initiate commerce flows, and the system has to treat that as a normal input.”

This is a massive undertaking. It implies a fundamental rethinking of what constitutes a valid payment instruction. Today, it’s typically a credit card number, a bank account, or a digital wallet. Tomorrow, it could be a request from a personal AI assistant, a smart contract, or an automated trading bot. Stripe’s move here is strategic; by defining the protocol, they position themselves as the plumbing for this new wave of AI-driven commerce. They’re making AI systems economically native, which is a fancy way of saying they’re building the rails for AI to actually spend money in the real world.

The Authorization Paradox: From Gatekeeper to Interpreter

This shift forces a profound reevaluation of existing payment infrastructure. Authorization, for instance, can no longer be just a binary yes/no. With agentic systems, authorization engines will need to become interpreters. They’ll need to understand the nuances of the AI agent’s request – its history, its predicted behavior, its trust score – not just whether the associated credit line is sufficient. This requires richer data streams and more sophisticated fraud detection models that can look beyond simple credential verification to assess the intent and context behind the transaction. It’s a move from a static gatekeeper to a dynamic, context-aware analyst.

Credit Reimagined: Dynamic, Per-Transaction Adjustments

And then there’s credit. Traditional credit lines are often fixed, with periodic reviews. Agentic commerce hints at a future where credit is far more fluid, adjusted per transaction based on the real-time risk assessment of the agent and the specific purchase. Imagine an AI agent negotiating micro-loans for individual purchases, or a system that can dynamically adjust credit limits based on an AI’s proven track record of responsible spending. Affirm, already a leader in Buy Now, Pay Later (BNPL), is likely watching this space closely, as agentic AI could transform its own underwriting processes and customer offerings.

The Infrastructure Backbone: Carrying Context, Not Just Credentials

Underpinning all of this is the infrastructure. The pipes that carry payment data – the networks, the APIs, the databases – need to evolve. They must move beyond simply transmitting credentials and transaction amounts. They need to carry context. This means embedding metadata about the AI agent, the user’s intent, the risk assessment, and the dynamic credit adjustments directly into the transaction flow. This is where the analogy to OpenAI’s work becomes clear; they’re building the intelligence, and companies like Stripe are building the means for that intelligence to act in the commercial sphere.

This is more than just a technological upgrade; it’s an architectural paradigm shift. It’s about moving from a command-and-control model of payments to a more emergent, agent-driven one. The real question isn’t if this will happen, but how quickly the existing players will adapt, and who will lead the charge in building this future. The gap between a user’s desire and the completed transaction is shrinking, and AI agents are the architects of that convergence.

🧬 Related Insights

- Read more: Meta’s Stablecoin Gamble: A Digital Echo or a New Dawn?

- Read more: Credit Scoring Innovation: Beyond FICO and Traditional Credit Bureaus

Frequently Asked Questions

What does agentic commerce actually do?

Agentic commerce uses artificial intelligence to make the entire payment process more autonomous and intelligent. AI agents can understand a customer’s intent, initiate transactions, and even dynamically manage credit, blurring the lines between thought and execution.

Will this make payments more expensive?

Potentially, the initial development and integration of these complex AI systems could lead to higher costs. However, the long-term goal is to increase efficiency, reduce fraud, and automate processes, which could ultimately lead to lower transaction costs for consumers and businesses through greater scale and reduced manual intervention.

How does this differ from current online payments?

Current online payments are largely driven by explicit user commands (clicking ‘buy’). Agentic commerce allows for implicit intent to be translated into action by AI agents on behalf of users, often without direct, moment-to-moment user intervention for every step. It introduces a layer of autonomous decision-making into the payment flow.