So, the Financial Conduct Authority — bless their bureaucratic hearts — have decided it’s time to throw some more official-sounding letters at the wall. CREDO. Asset Finance. Sounds important, right? Like some secret handshake for companies that deal in… well, stuff you borrow money to buy. For those of us who’ve been watching this fintech circus for two decades, it smells suspiciously like the same old song and dance: regulation that’s always a few steps behind the innovation it claims to shepherd, all while ensuring consultants and compliance officers eat well.

Here’s the thing about these new frameworks, especially when they target something as broad as asset finance. You’ve got everything from car loans to heavy machinery leasing under this umbrella. The FCA’s press materials — which, let’s be honest, are usually drier than a Silicon Valley startup pitch deck after Series B — talk a big game about ‘effective supervision’ and ‘consumer protection’. Lofty goals, no doubt. But here’s the real question that always hangs in the air like a bad IPO valuation: who is actually paying for this, and who benefits beyond the regulators themselves?

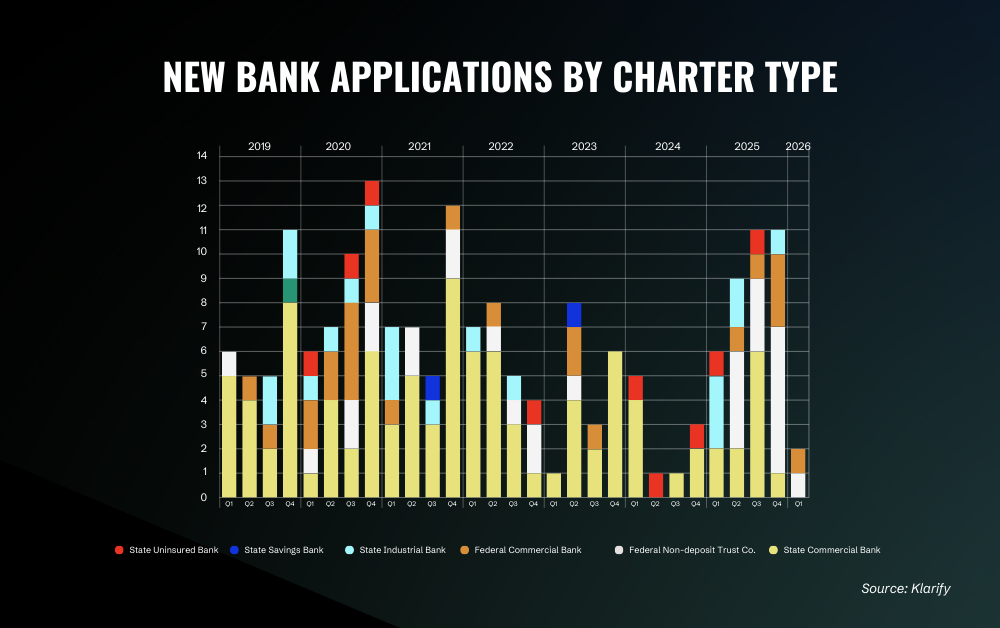

CREDO, apparently, stands for something. It’s supposed to provide a structured approach for firms applying for authorization or variation of permissions. Think of it as a standardized application checklist, but with more jargon. They want firms to understand their obligations, identify risks, and demonstrate how they’re meeting standards. All perfectly reasonable, on paper. But the devil, as always, is in the execution. And in the cost.

Is CREDO a Boost or a Burden?

The FCA claims this will make the authorization process smoother. Smoother? For whom? For the fintech startups that are already scraping by, juggling product development with existential dread? Or smoother for the established players who have armies of lawyers and compliance teams already on retainer, who can absorb these new requirements with a shrug and a slightly larger budget line item?

For the burgeoning asset finance fintechs, this looks less like a helping hand and more like a fresh set of hurdles. Every new piece of regulation, every requirement to ‘demonstrate understanding’ or ‘identify risks’ translates into billable hours for external consultants. And don’t even get me started on the internal resources diverted from actual business building to paper-shuffling and form-filling.

“CREDO provides a clear framework to help us supervise firms effectively, ensuring that those operating in the asset finance sector meet our standards and protect consumers.” – FCA Statement

Effective supervision is one thing. Making it so expensive to even get in the door that only the already-funded can afford it is another. This feels like a classic case of regulatory creep, dressed up in the language of consumer welfare and market integrity. The FCA is essentially saying, ‘We’re here to help you by making it harder for you to operate.’

The Unseen Costs of Compliance

This isn’t just about the application fees, although those can be hefty enough for a bootstrapped venture. It’s about the ongoing operational overhead. Imagine a small team that’s built a slick app for equipment leasing. Now, they have to prove to the FCA that they’ve thought through every single potential failure mode, that their data security is Fort Knox-level, and that their marketing materials won’t accidentally mislead a pensioner into leasing a tractor they don’t understand. It’s exhausting.

And the real irony? The companies that truly need the most oversight are often the ones finding the most creative ways to circumvent it. Meanwhile, the innovative, upstanding firms get bogged down in bureaucracy. We’ve seen this movie before with PSD2, with open banking initiatives that promised the moon and delivered a somewhat dusty crater. The intent is usually noble; the outcome often favors the incumbents and the professional services industry.

My take, after two decades of this predictable cycle? CREDO is likely to become another bureaucratic gatekeeper. It’ll make it easier for the FCA to tick boxes, and it’ll provide a steady stream of income for compliance consultants. For the truly disruptive fintechs trying to make asset finance more accessible and efficient, it’s just another complex maze to navigate. The ‘best experience’ on their website, as Crowdfund Insider might put it, will likely be for the lawyers who help firms fill out the forms.