Spotlights flicker in a dimly lit D.C. conference room as a fintech exec clutches her phone, heart pounding over a regulator’s email: preliminary approval for a full bank charter.

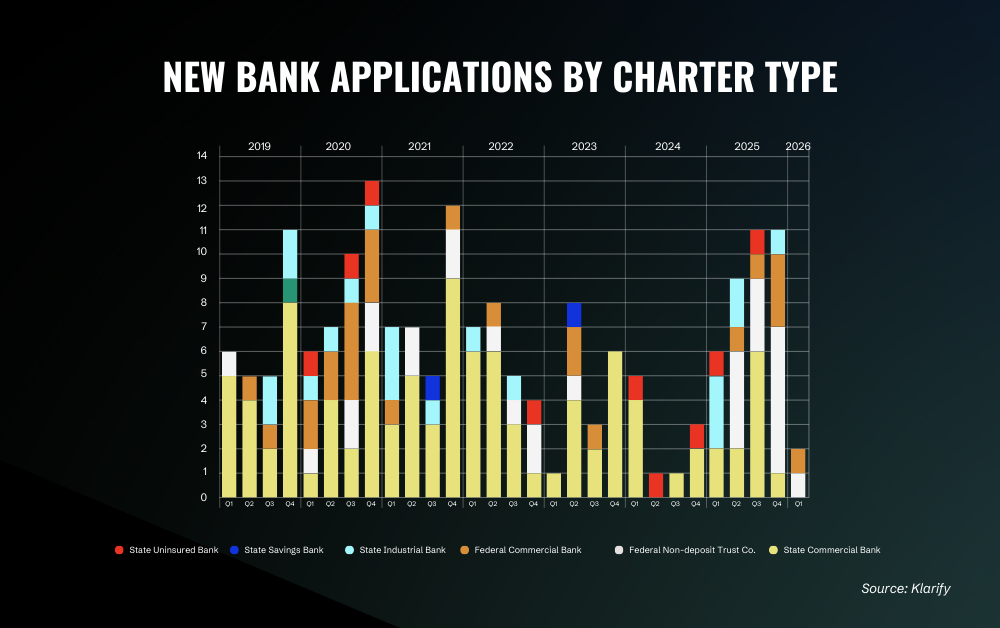

That’s the scene repeating across Silicon Valley boardrooms right now, in this bank charter gold rush that’s turning fintech dreams into steel-and-compliance reality. Barely a year into the Trump era, and we’re drowning in applications—over 30 in the pipeline, after zilch during Biden’s four-year freeze. It’s not hype; it’s a seismic shift, like the moment railroads got chartered en masse in the 1800s, sparking an industrial explosion that redrew America’s map.

Why the Hell Is This Happening Now?

Biden’s regulators? Zero tolerance for anything smelling like risk. Michele Alt from Klaros Group nails it:

“During the Biden administration, the regulators applied effectively a ‘zero tolerance for risk approach’ to new bank formation. Which, if you have no appetite for risk, no one’s going to get through.”

That iron-fisted stance didn’t kill risk—it shoved it into shadowy sponsor-bank deals, where watchdogs couldn’t peek. Fintechs chafed under the scrutiny, their bank-as-a-service gigs turning into regulatory minefields. Now? Trump’s team is flipping the script, handing out preliminary nods like candy at a parade.

But here’s my take, the one you won’t read in the press releases: this mirrors the 1996 telecom deregulation, when the internet finally busted free from Ma Bell’s grip. Back then, new carriers flooded in, slashing costs and birthing e-commerce giants. Today’s charter wave? It’ll unleash AI-native banks—think models that predict your cash flow before you spend it, embedding neural nets into every deposit. Corporate spin calls it ‘innovation’; I call it the platform shift that makes legacy banks look like steam engines.

And yeah, the numbers don’t lie. From zero to sixty, as experts put it—applications pouring in weekly.

Look, preliminary approval’s just the pickaxe. The gold’s buried deep.

House Permits or Actual Front Doors?

David Portilla at Davis Polk drops the perfect analogy—getting that initial nod is like snagging building permits for your dream home. You can start hammering, sure, but don’t pop the bubbly yet. Certificate of occupancy? That’s 18 months out, minimum, crammed with infrastructure builds, policy overhauls, management hires, and pre-opening exams that’d make a drill sergeant sweat.

“If you think of chartering a bank like building a house, getting your preliminary conditional approval is like getting all of your permits that let you start construction. Then, much later, you have to get your certificate of occupancy, which means you can move in.”

Mike Nonaka from Covington & Burling chimes in: it’s a milestone, not a finish line. Regulators aren’t asleep—they’re watching every nail hammered. Not every permit-holder moves in; some blueprints crumble under scrutiny.

Three phases, per Alt: application vetting (plans, money, bosses), the brutal in-organization grind, then endless supervision post-launch. Critics whine about ‘quick approvals’? They’re missing the marathon ahead.

Thrilling, isn’t it? Fintechs aren’t just playing banker—they’re engineering the future.

Charter Poker: Which Hand Wins?

Crypto outfits? Sniffing national trust charters like sharks to blood—no FDIC hassle, no Fed oversight on parent ops. Smart. Industrial loan companies (ILCs)? Same dodge on holding company rules, but skimpier product menus. It’s a high-stakes calculus: dream services versus regulatory chains.

Portilla breaks it down—you map your offerings, tally the rulebook weight, decide if the juice is worth the squeeze. Legacy banks sneer from afar, but here’s the wonder: these charters birth hybrid beasts, fusing fintech speed with bank muscle. Imagine deposit apps that evolve via machine learning, spotting fraud in real-time dreams.

My bold call? By 2027, we’ll see the first AI-first chartered bank, processing loans via predictive models that laugh at human underwriters. Trump’s rush isn’t politics—it’s the spark for banking’s Cambrian explosion.

Not all will pan out. Some’ll fizzle in the ‘in org’ phase, teams fracturing under pressure. But survivors? They’ll mine veins incumbents can’t touch.

And the incumbents—watch ‘em scramble. Partnerships incoming, or panic.

Short para for punch: Game on.

Will These Fintech Banks Survive the Build?

Skeptics say yes, but with asterisks. Alt’s blunt: scrutiny ramps up, not down. Nonaka sees direct regulator chats as a fintech win—cut the sponsor-bank drama.

Yet risks lurk. Talent wars for C-suite pros versed in both code and capital requirements. Tech stacks that scale without crashing under Fed eyes. It’s messy, human—delays, pivots, maybe a few flameouts.

But oh, the payoff. A chartered fintech isn’t a startup anymore; it’s infrastructure, wired into the payments grid, rails humming with velocity.

Picture deposits flowing like rivers, AI damming floods before they crest. That’s the future we’re building, one approval at a time.

We’ve waited years. Now? The rush.

Why Should You Care About Fintech Charters?

Consumers get better apps—faster loans, slicker wallets. Investors? Spot the winners early; charters signal seriousness. Devs? APIs galore from new players.

Legacy banks? Adapt or atrophy. This gold rush redraws the map, much like railroads birthed modern America.

Energy here—it’s palpable. Fintech’s not knocking anymore; it’s inside, swinging the hammer.

🧬 Related Insights

- Read more: Coinbase’s x402: Crypto’s AI Payment Moonshot or Mirage?

- Read more: $100 Trillion Handover: Will Stablecoins Actually Kill Legacy Payments?

Frequently Asked Questions

What’s a preliminary bank charter approval?

It’s the green light to start building your bank—permits issued, but no doors open yet. Think 18+ months of heavy lifting ahead.

How long until these fintech banks launch?

Typically 18-24 months post-prelim, navigating exams, hires, and infrastructure. No shortcuts.

Best charter for crypto companies?

National trust charters dodge FDIC and Fed parent oversight—perfect for exchanges staying nimble.