Are we witnessing the quiet assimilation of crypto by legacy finance? CaixaBank, Spain’s third-largest bank, just received its crypto-asset service provider (CASP) license under the EU’s Markets in Crypto-Assets Regulation (MiCAR). This isn’t just another bank dipping its toes into digital assets; it’s a powerful statement, and it follows closely on the heels of its major Spanish rivals, BBVA and Santander’s Openbank. The implications for the future of both traditional banking and decentralized finance are, frankly, enormous.

The Streamlined Path to Legitimacy

It’s easy to look at this headline and think, “Okay, banks are offering crypto services.” But the real story, the architectural shift, lies in how they’re doing it. MiCAR, while a landmark piece of legislation for consumer protection and market integrity, also offers a surprisingly efficient on-ramp for established credit institutions. Unlike fintech startups that might face years of rigorous vetting and complex licensing across multiple jurisdictions, banks have a… well, a streamlined path. They essentially need to give their regulator 40 days’ notice. Forty days. It’s less a fresh application and more an announcement of intent, leveraging their existing regulatory standing.

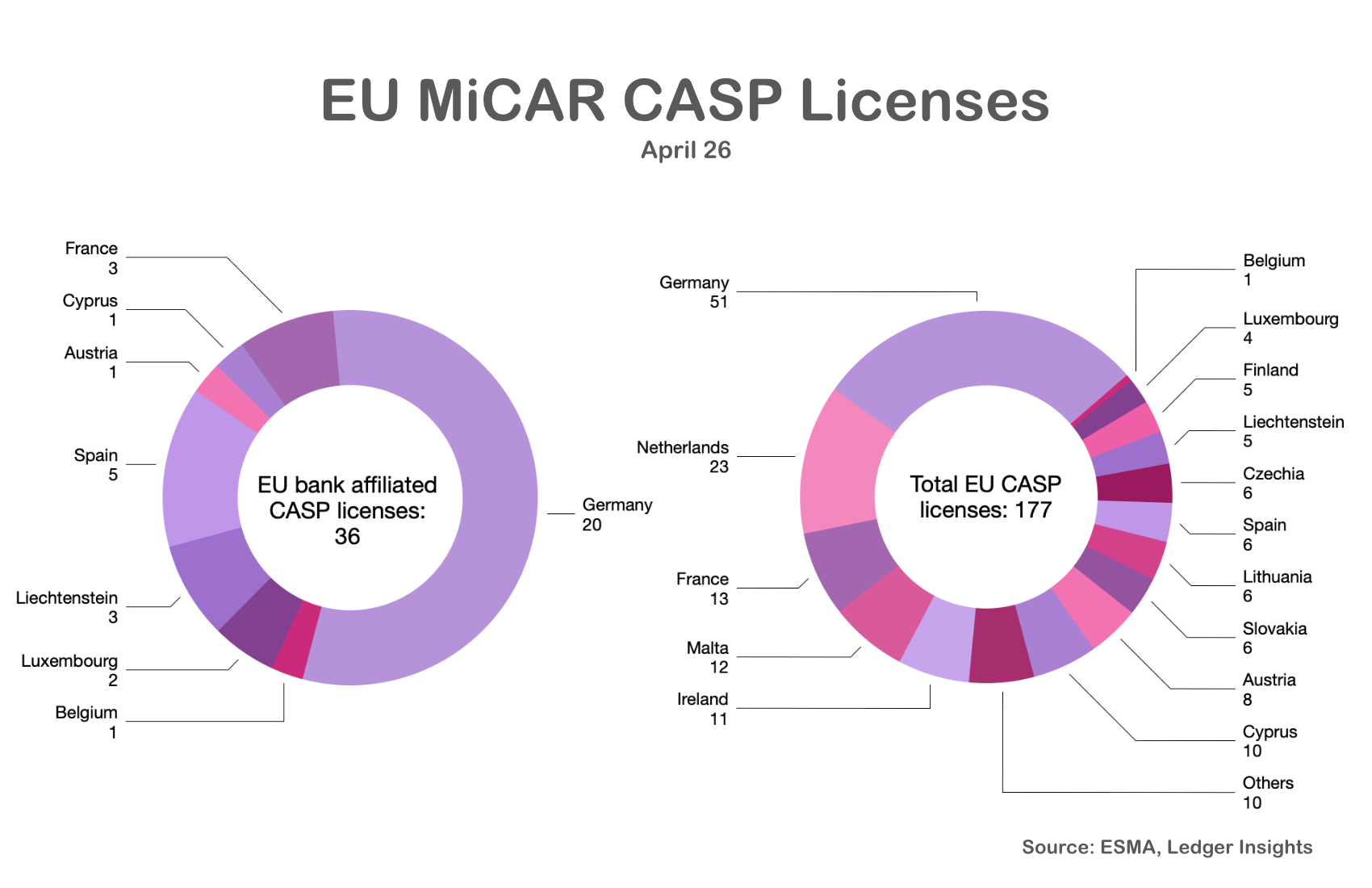

This architectural advantage for banks — the ability to pivot into a new asset class with relative speed and minimal regulatory friction (compared to a new entrant) — is precisely why we’re seeing this surge. They’re not building new rails from scratch; they’re adapting existing, highly trusted infrastructure. The article notes that out of 177 CASP licenses awarded so far, a significant 36 are held by banks. This isn’t an accident. It’s a consequence of regulatory design that, intentionally or not, rewards incumbents.

Beyond Custody: What’s Actually Being Offered?

So, what does CaixaBank’s license actually cover? It’s not just about holding Bitcoin in a digital vault. The license spans crypto custody, order transmission and execution, and client transfers. This means they’re building out the plumbing to not only store digital assets but to facilitate trades and move them around on behalf of their customers. They’re already dabbling with Bitcoin ETPs through their digital platforms and are part of a consortium developing a euro-linked stablecoin. This isn’t a casual exploration; it’s a calculated integration.

The core question isn’t if banks will offer crypto services, but how they’ll differentiate and what their presence will mean for the existing decentralized ecosystem. Will they become the custodians of choice for risk-averse retail investors? Will their scale allow them to negotiate better trading fees than many decentralized exchanges? The power asymmetry here is palpable. Traditional banks bring brand trust, vast customer bases, and established compliance frameworks. These are not trivial advantages in an industry often characterized by its perceived opacity and volatility.

The “Why Now?” and the Underlying Fear

Why this sudden acceleration? Several factors are at play. Firstly, the regulatory clarity MiCAR provides is a massive catalyst. Before, it was a Wild West with fragmented rules. Now, there’s a defined framework. Secondly, the sheer growth and institutional interest in digital assets can no longer be ignored. Banks, often criticized for being slow to innovate, are acutely aware of the risk of obsolescence. If their customers are moving wealth into crypto, and traditional assets are yielding less, the pressure to adapt is immense.

But let’s not be naive. This move also speaks to a deep-seated understanding, perhaps even a fear, within traditional finance. They see the potential disruption of DeFi, the rise of new financial intermediaries, and the erosion of their gatekeeper status. By integrating crypto services under their umbrella, they’re not just adopting a new product; they’re attempting to regain control of the narrative and the flow of capital. They are, in essence, building their own walled gardens within the nascent digital asset landscape. It’s a strategy of co-option.

The Architecture of Trust: Bank vs. Blockchain

This brings us to a fundamental architectural question: what constitutes trust in finance? For centuries, it’s been centralized institutions, regulators, and physical security. Blockchain proponents argue for trustless systems built on cryptography and distributed ledgers. What we’re seeing now is a fascinating hybrid where the architecture of trust is being rebuilt, or at least significantly influenced, by the established players. Banks are betting that their existing architecture of trust—their brand, their regulatory relationships, their physical presence—will be more palatable to the mainstream than the pure, permissionless ethos of DeFi.

CaixaBank’s move, alongside BBVA and Santander, signals that the era of purely decentralized finance might be giving way to a more hybridized model. It’s a model where the familiar structures of traditional banking provide the access and perceived safety, while the underlying assets are digital and blockchain-based. This is not a hostile takeover, but a strategic acquisition of market share and relevance. The long-term implications for how we store value, transfer assets, and manage risk are profound. The age of the bank-issued stablecoin, the bank-custodied NFT, and the bank-facilitated crypto trade is dawning.

🧬 Related Insights

- Read more: Instant Payments Get Ironclad Fraud Shields—Your Wallet Just Got Safer

- Read more: AI Fitting Rooms: Retail’s Desperate Bid to Kill the Returns Plague

Frequently Asked Questions

What does a CASP license under MiCAR actually allow a bank to do? A CASP license allows a bank to legally offer services such as crypto custody, the transmission and execution of orders for crypto-assets, and client transfers of crypto-assets within the EU.

Will this mean I can buy Bitcoin directly from my CaixaBank app soon? CaixaBank has stated it plans to roll out services in the coming months, suggesting users will likely be able to access these crypto offerings through their existing digital banking platforms or associated apps.

Is this a sign that traditional banks are fully embracing crypto, or just complying with new regulations? While MiCAR mandates certain standards, the proactive pursuit of CASP licenses by major banks like CaixaBank, BBVA, and Santander suggests a strategic business decision to integrate crypto services, likely driven by market demand and the desire to retain customers in the evolving financial landscape, rather than mere compliance.