The faint buzz of a smartphone screen, momentarily illuminated as a credit card hovers nearby. It’s a scene we’ll soon see a lot more of.

And here’s the thing: this isn’t just another incremental upgrade in the world of fintech. We’re talking about a fundamental platform shift, the kind that ripples through industries and redefines how businesses operate. Adyen and Starling Bank, two giants in their respective fields, have just teamed up to unleash a tap to pay feature directly within the Starling app, and it’s poised to be an absolute game-changer for the UK’s small and medium-sized businesses (SMEs).

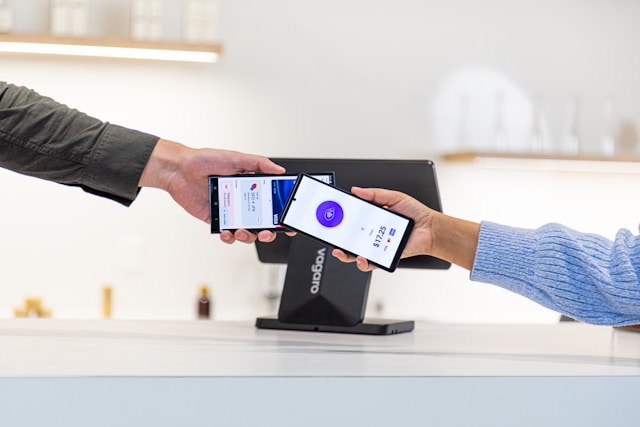

Think about it. For years, accepting card payments meant wrestling with bulky hardware, dealing with contracts, and navigating a labyrinth of fees. It was a significant barrier, especially for nimble startups and sole proprietors just trying to get off the ground. This new partnership? It’s like giving every small business owner a magic wand that turns their existing smartphone into a fully functional, secure payment terminal. Poof! No more extra boxes, no more complicated setups. Just download, configure, and start accepting payments in minutes.

This isn’t merely about convenience, though. It’s about democratizing access to modern payment infrastructure. By embedding Adyen’s sophisticated processing power directly into Starling’s user-friendly banking app, they’ve created an experience so streamlined it feels like pure wizardry. From the moment a business signs up to the daily settlement of funds, everything happens within that single app. No more juggling multiple platforms or waiting days for money to clear. Funds land in your Starling account the very next day, ready for you to reinvest or, you know, grab a much-deserved coffee.

The tech itself is elegantly simple, leveraging the NFC technology that’s already in most of our pockets. A quick tap, a secure PIN entry if needed (which also happens right there on the phone, mind you), and the transaction is done. And importantly, for all the privacy-conscious folks out there, Adyen assures us that sensitive data – the kind that keeps cybercriminals up at night – isn’t lingering on the device or some distant, vulnerable server.

But wait, there’s more! Starling isn’t resting on its laurels. They’ve also announced plans to weave payment links into their free invoicing tool later this year. Imagine sending an invoice and having a direct link for customers to pay via card or mobile wallet. It’s about making the entire get-paid cycle feel less like a chore and more like a natural extension of doing business.

What’s truly remarkable here is the accessibility. There’s no monthly subscription fee for the tap-to-pay feature itself. Businesses are only charged a simple, flat rate per transaction. This is the kind of pricing model that speaks directly to the heart of SME profitability, removing uncertainty and predictable overhead.

“Tap to pay technology removes traditional barriers to accepting card payments by turning a smartphone into a secure, user-friendly payment terminal. By combining Adyen’s financial technology and banking capabilities with Starling’s UK banking infrastructure, we are helping UK SMEs bridge the gap between their payment processing and daily financial management.”

This is Adyen UK managing director Nicole Olbe, and she’s hitting the nail on the head. It’s not just about accepting payments; it’s about integrating that process so tightly with core financial management that it becomes almost invisible. And that’s where the real power lies for businesses.

Starling director of customer solutions Sami Kade echoed this sentiment, emphasizing the bank’s commitment to making small businesses “good with money.” And what better way to be good with money than to make it easier to receive it in the first place? Redirecting energy from payment logistics to actual business growth is the ultimate goal, and this partnership is a massive stride in that direction.

The True Magic: Beyond the Tap

Here’s my unique insight: while the tap-to-pay functionality itself is undeniably cool, the real story is the integration into a digital bank. Historically, payment processing and banking have been separate beasts, often with competing interests and clunky interfaces. Adyen and Starling are smashing that wall down. This isn’t just a payment feature; it’s a banking feature that enables payments. For SMEs, this means their daily financial management is now intrinsically linked to their ability to transact. It’s a virtuous cycle, a true platform play where the core banking experience is enhanced by best-in-class payment capabilities, and vice-versa. This level of smoothly integration is what separates fleeting trends from lasting platform shifts.

Think of it like the early days of the internet. Suddenly, information was accessible. Then came e-commerce, transforming how we bought and sold. Now, with AI acting as the foundational layer for so much innovation, we’re seeing this same kind of explosive, platform-level change in finance. Adyen and Starling are essentially building one of the foundational pillars for this new era of hyper-integrated financial services for businesses.

Why Does This Matter for UK SMEs?

For entrepreneurs and small business owners across the UK, this means a more agile, accessible, and cost-effective way to do business. It reduces friction at the point of sale, potentially increases sales by capturing impulse buys that might have been lost without immediate payment options, and simplifies financial administration. It’s a powerful signal that the tools of modern commerce are no longer exclusive to large corporations; they’re increasingly available to everyone, right from their pocket.

🧬 Related Insights

- Read more: TechCrunch Disrupt 2025 Day 3: AI Hype Peaks as Winners Emerge

- Read more: Coinbase Stablecoin Fund Bets on Tokenized Shares

Frequently Asked Questions

Will this replace traditional card machines?

It’s likely to significantly reduce the need for them, especially for businesses that don’t require high-volume, stationary payment points. The flexibility of a smartphone is hard to beat for mobile businesses, pop-up shops, or service providers on the go.

Is it secure to take payments on a smartphone?

Yes, Adyen and Starling emphasize that the technology uses secure NFC protocols and ensures that sensitive data is not stored on the device or on their servers, adhering to industry-standard security practices.

How quickly will I get my money?

Funds from tap-to-pay transactions are deposited into the business’s Starling account the following day.