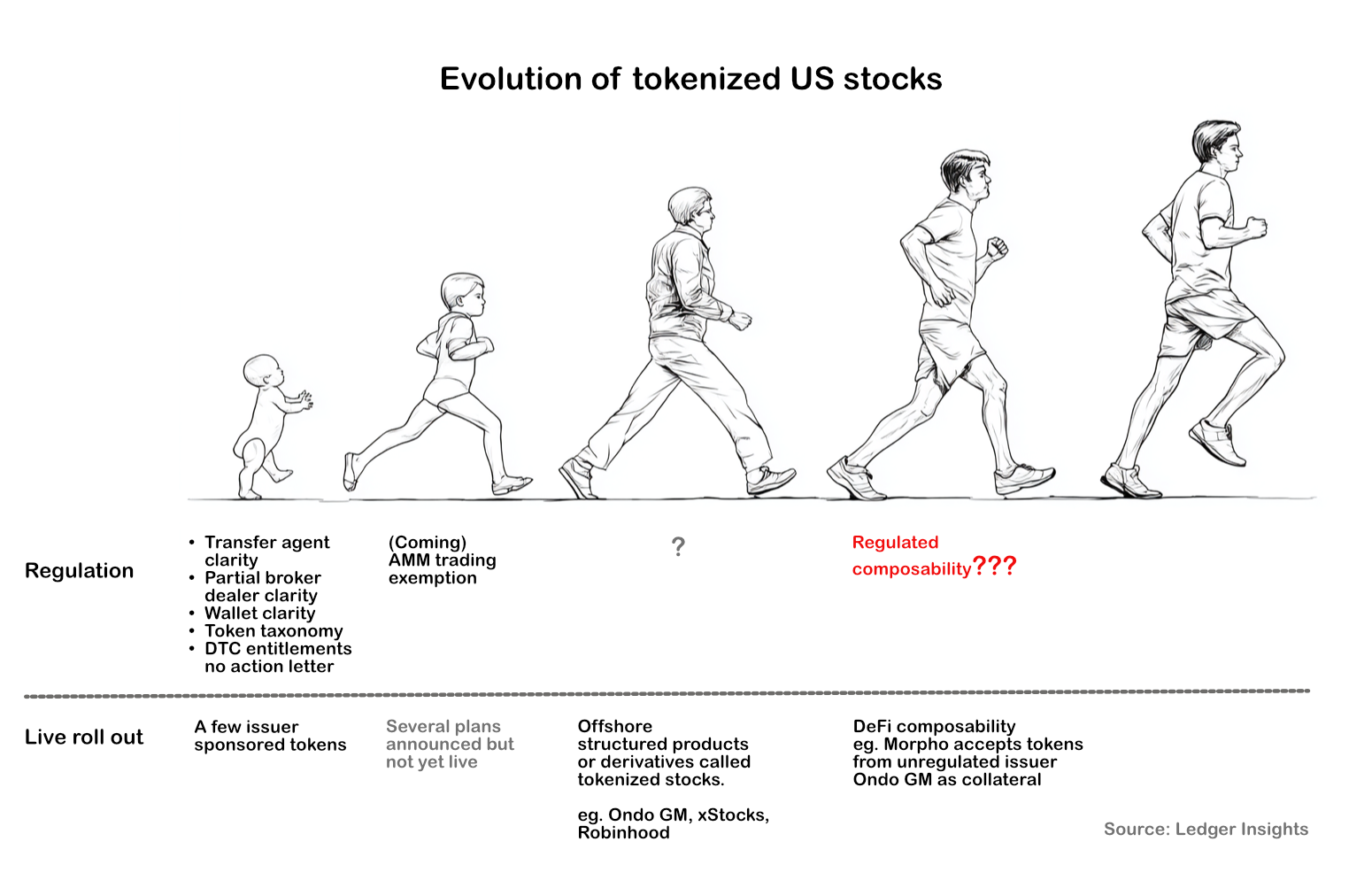

Ever wonder if all this talk about tokenization is just a fancy way of saying ‘we moved our spreadsheets to the cloud’? Because honestly, sitting here, twenty years deep in the Silicon Valley circus, it often feels that way. We hear about distributed ledgers this, smart contracts that, all promising to revolutionize finance. But dig a little, and what do you find? Often, it’s just the same old financial products, repackaged for crypto-native investors who probably have too much Bitcoin anyway.

Now, a couple of folks over in the UK, Stephen Whyman (ex-BlackRock, Fidelity International) and Dr. Ian Hunt (industry consultant), have dropped a paper that’s basically saying what a lot of us have been muttering under our breath: “Replicating Legacy is Squandering the Promise of Tokenisation.” Their beef? The current financial system is a labyrinth of asset-specific, product-specific silos. Think separate regulations, separate tech stacks, separate business units for stocks, bonds, derivatives. It’s an operational nightmare that bleeds money. And tokenization, as it’s currently practiced, is just building a shinier, more expensive version of that same mess.

Are We Just Digitizing the Same Old Paperwork?

Here’s the radical part, and honestly, it’s so simple it’s almost insulting we haven’t seen it widely adopted. Instead of encoding every single complex term, condition, and regulatory nuance into a bespoke smart contract for each individual asset class—a task that sounds like building a skyscraper with toothpicks—Whyman and Hunt propose a stripped-down approach. They reckon most financial assets can be represented using just two fundamental token types: a token of title and a token of entitlement.

A token of title? That’s just your ownership stake, plain and simple. Own a building? You get a title token. Own a share of Apple? Title token. A commodity? Yep, title token. Then there’s the token of entitlement. This is where the future payments and obligations live. Think coupon payments on a bond, dividend payouts from that Apple stock, or the obligation to deliver a stock on a certain date. It’s elegant, really.

“Their proposal is radical in its simplicity. Rather than encoding the full terms, conditions, processes and regulations of each asset class into bespoke smart contracts, they argue that virtually all financial assets can be represented using just two types of tokens.”

This isn’t just theoretical musing. The paper apparently walks through how your standard fixed-rate bond, your pesky interest rate swaps, even options contracts—all those financial gizmos that make compliance officers sweat—can be built by just arranging clusters of these two token types. And the real kicker? New asset classes or innovative financial products wouldn’t need a whole new technological infrastructure or a fresh batch of special-purpose tokens. Just new configurations of the same two basic building blocks.

Who’s Actually Making Money Here?

This is where my cynical veteran reporter radar starts pinging like crazy. Because while Whyman and Hunt are talking about elegant technical solutions and the democratization of finance, I’m looking at the VCs writing checks and the established financial players pouring money into these tokenization platforms. Are they really trying to build this elegant, composable future, or are they just trying to slap a blockchain sticker on their existing revenue streams? My money’s on the latter.

The current approach, where every tokenized fund or derivative requires its own specialized smart contract development and compliance layer, is a goldmine for consulting firms and blockchain development shops. It’s complex, it’s expensive, and it keeps the big players in their comfortable, familiar silos. The Whyman-Hunt model, by contrast, aims to reduce that complexity. It’s a threat to anyone making a tidy profit off the status quo.

Consider the historical parallel: the early days of the internet. We had proprietary networks, walled gardens, and companies charging a fortune for access. Then came open standards and protocols that allowed anyone to connect and build. That democratized access and exploded innovation. The Whyman-Hunt paper feels like that moment for tokenization. But will the incumbents, who’ve spent decades building their legacy empires on complexity, embrace a model that aims to simplify everything?

I doubt it. They’ll likely pay lip service, fund a few pilot projects that go nowhere, and continue to sell their ‘digitized legacy’ solutions. The real question isn’t whether tokenization can be composable; it’s whether the people who hold the reins of power and profit in finance want it to be.

The Bottom Line

Look, the potential is there. Tokenization, when done right, could unlock unprecedented efficiency and liquidity. It could lower costs and create entirely new investment opportunities. But right now, for many, it’s a solution in search of a problem, or worse, a PR exercise to appear technologically forward-thinking while milking the same old revenue streams. The UK experts have laid out a compelling blueprint for what tokenization should be. The real test will be whether the industry, bogged down by its own entrenched interests, has the appetite for genuine change or just another shiny digital distraction.

🧬 Related Insights

- Read more: Circle Co-Founder’s Catena Labs Raises $30M for AI Bank

- Read more: Fintechs Chip Away at Banks in 2026

Frequently Asked Questions

What does tokenization composability mean? Tokenization composability refers to the ability to combine different tokenized assets and financial instruments to create new, more complex financial products, much like building with LEGO bricks, without needing custom infrastructure for each new combination.

Will this simplify financial markets? The proposed two-token model aims to significantly simplify financial markets by reducing the need for asset-specific infrastructure and complex smart contracts, potentially lowering costs and increasing efficiency.

Is this just about crypto investors? While current tokenization efforts often target crypto-native investors, the experts argue that a composable approach has the potential to benefit traditional finance and a broader range of investors by making financial products more accessible and adaptable.