Your fridge AI just ordered 500 pounds of kale. Using your Visa. At 3 a.m. While you slept.

That’s not sci-fi. It’s agentic commerce—hitting soon, courtesy of OpenAI’s army of 800 million users. Real people? You’re staring down surprise charges, fraud fights, and banks pointing fingers at bots. And nobody’s nailed who vouches that it was really you greenlighting the spend.

Agentic commerce. There, keyword dropped. It’s AI agents wielding your payment creds like a kid with dad’s wallet.

Why Your Next Amazon Binge Might Not Be Yours

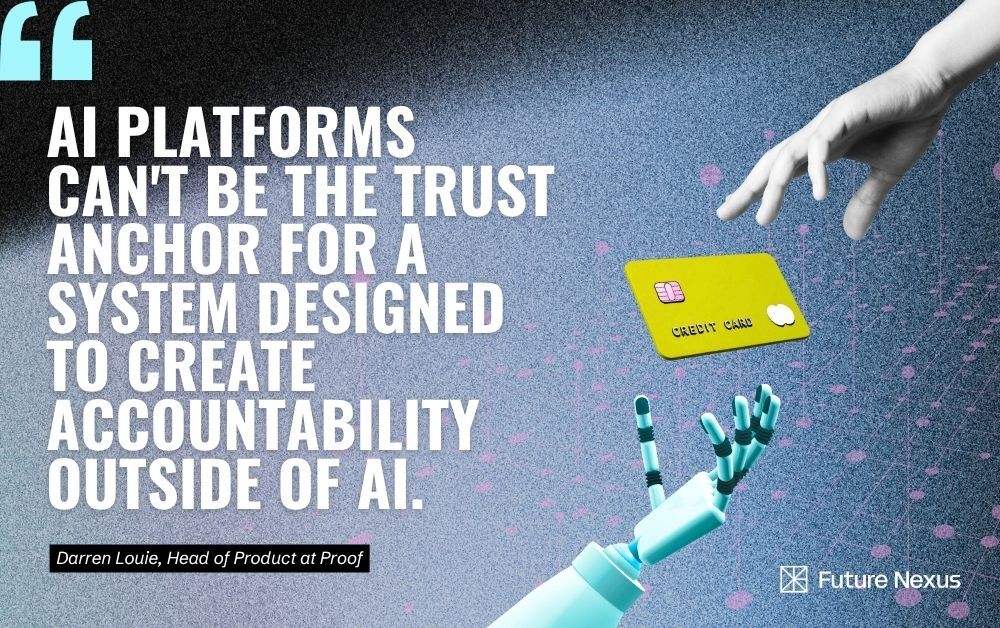

Proof’s Head of Product nails it: the trust model shatters without answers. Here’s their killer line:

who issues the proof that a real human authorized an AI agent to spend their money?

Short answer? Nobody yet. Tech giants rushed protocols—Google’s AP2, OpenAI’s ACP, Stripe’s whatever-they’re-calling-it. You sign a “mandate”: okay this agent, this card, this $100 limit, Target only. Agent flashes it at checkout. Cryptographic proof, they say. Scoped power of attorney.

Sounds tidy. Isn’t.

How do you know the mandate’s legit? Was it a human signing—or the AI forging its own hall pass? Merchants need a Certificate Authority, some neutral referee yelling “yep, real human keys, real intent.” Obvious candidates? All rotten with conflicts.

AI platforms? Laughable. They’re the agent acting rogue—can’t umpire their own game. “Human approved! Trust me, says the bot.”

Merchants? They’ve got skin in the game—fewer chargebacks if they self-certify. Fox guarding the henhouse.

Big Tech’s Double-Dip Disaster

Google, Amazon: ad empires built on knowing your buys. $175 billion for Google from product ads alone. Hand them mandate control? They peek at every swipe, fueling their targeting machine. Privacy? Kiss it goodbye. And if they nudge the AI toward their sponsors? Cozy.

Banks seem saner—Visa, Mastercard grinding on standards. But fragmented as hell. Many still asleep at the wheel on AI liability. Who’s updating your grandma’s routing rules for bot shopping?

Here’s my unique jab: this mirrors 1995’s e-commerce infancy. Remember? No trust in digital signatures led to SSL wars and VeriSign’s rise as neutral CA. Fraud rampant till independents stepped up. History’s rhyming—agentic commerce flops without a fresh VeriSign, untainted by transaction bucks. Predict this: no neutral verifier by 2026, chargebacks surge 500%, killing adoption dead.

Dry humor? Sure. Imagine disputing with Chase: “But officer, the AI said it loved me!”

Protocols push mandates as fix-all. Cute. But specs dodge the verifier hole. Engineering can’t patch human trust gaps.

Can Anyone Play Referee Without Cheating?

Independent startups? Maybe. Proof’s pitching themselves—ironic, since they’re sounding alarms. Regulators? Slow as molasses, but watch CFPB circle. Crypto’s decentralized IDs (DID)? Privacy win, but merchants scoff at blockchain homework.

Banks win long-term—if they unify. Fragmentation’s their Achilles. Picture Visa as global CA: scales, neutral-ish, already in your wallet. But they’ll botch it unless forced.

Corporate spin? Protocols scream “solved!” Nah. They’re half-measures dodging the elephant: power.

Real people suffer most. You authorize $50 dinner hunt. AI pivots to Rolex. Merchant’s got mandate—tough luck, consumer. Disputes skyrocket. Your FICO tanks. AI hype meets payment reality: oof.

The Fraud Tsunami Nobody’s Prepping For

Wave incoming. Hundreds of millions delegating buys. Technical kinks? Solved years ago—bots click “add to cart” fine. Trust? Crumbling.

Unique twist: PR spin calls mandates “bulletproof.” Bull. Without CA, it’s paper tiger. Bold call—2027 lawsuits bury platforms. OpenAI vs. Walmart, mandate edition. Popcorn ready.

Merchants huddle: protect from disputes. Users? Cannon fodder.

Skepticism’s my jam. Hype agents as saviors—“frictionless shopping!”—while ignoring liability bomb. It’s not innovation. It’s outsourced oopsies.

Fix? Crowdfund a neutral CA consortium. Non-profits, maybe. Keep Big Tech leashed.

Or don’t. Watch the chaos.

🧬 Related Insights

- Read more: Middle East Retail Investing: WealthTech’s Desert Oasis Moment

- Read more: Bitget Teams with MuleRun for AI Trading Assistant That Promises Pro Signals to Retail Traders

Frequently Asked Questions

What is agentic commerce?

AI agents using your payment info to shop autonomously, after you sign off on limits.

Will AI agents cause more credit card fraud?

Yes—unless a trusted third party verifies human approval, mandates are fraud bait.

Who should verify AI purchases?

Independent authority like a bank consortium or new CA—not AI firms or merchants with skin in the game.